The recent updates regarding PMK 15 Tahun 2025 have sparked significant public interest and discussion about future regulations and policies.

As global trade tensions intensify and businesses face an increasingly complex economic landscape, Indonesia’s Ministry of Finance has streamlined tax audit timelines through PMK 15 Tahun 2025 (PMK 15/2025). This regulation responds to business needs for operational efficiency while maintaining strong tax compliance standards.

What PMK 15/2025 Changes for Indonesian Businesses

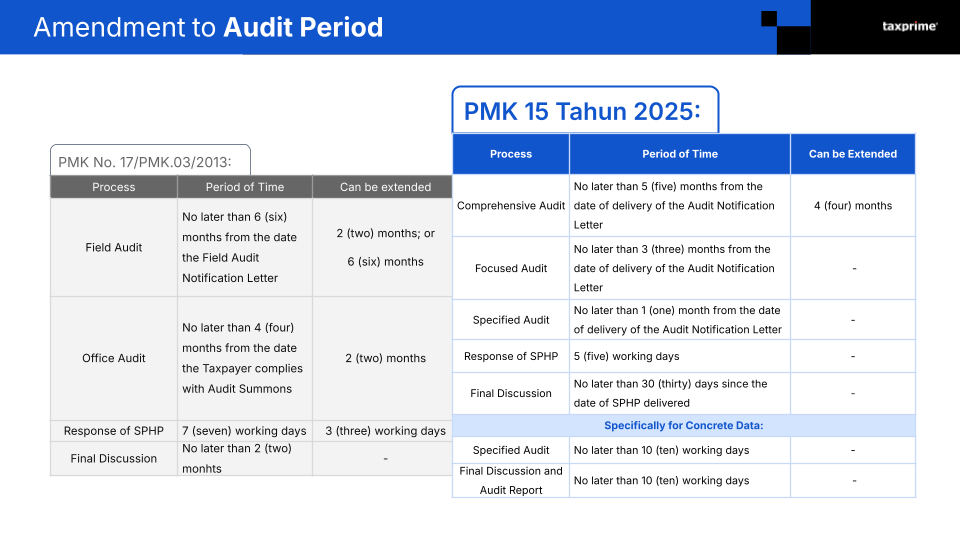

PMK 15 Tahun 2025 (PMK 15/2025) is Indonesia’s latest tax audit (pemeriksaan pajak) regulation from the Ministry of Finance, effective February 1, 2025. The regulation shortens tax audit duration with three audit categories. Comprehensive tax audits now have a maximum duration of 5 months, focused tax audits must conclude within 3 months, and specific tax audits are capped at 1 month. Compared to the previous PMK 17/2013 regulation, tax audits could extend up to 12 months, creating prolonged uncertainty that affected business planning and cash flow management.

PMK 15/2025 addresses a critical pain point for Indonesian businesses, particularly exporters and Value Added Tax (VAT) refund claimants. The shortened tax audit period helps companies manage working capital more effectively, make strategic investment decisions with greater confidence, and maintain competitive positioning in global markets (read our newsletter about the crucial points of PMK 15 Tahun 2025)

Impacts for Companies

VAT refund claimants experience the most immediate advantages from PMK 15/2025. Export-oriented businesses that regularly file VAT refund claims previously endured extended waiting periods while tax authorities completed audits, freezing working capital for months. The adjusted audit timeline means faster refund processing and improved cash flow.

However, the shortened timeline demands significantly higher compliance readiness. Companies must be audit-ready at all times, as tax authorities can now complete audits within compressed timeframes that leave little room for delayed responses or disorganized records. This requires implementing standardized documentation systems that categorize all tax-relevant transactions systematically.

Employee training also becomes critical for efficient engagement with tax auditors. Finance teams need to understand audit procedures, know which documents correspond to specific audit requests, and communicate effectively with tax authorities without unnecessary delays.

Strengthening Indonesia’s Investment Competitiveness in ASEAN

The improved tax administration system through PMK 15/2025 directly enhances Indonesia’s appeal as an investment destination within the Southeast Asian region. For multinational corporations and domestic investors seeking broader market opportunities, the shortened tax audit process represents a huge improvement. This change aligns with Indonesia’s broader economic reform agenda to create a more competitive business environment while preserving tax compliance.

The regulation exemplifies modern tax administration principles, balancing compliance enforcement by the Directorate General of Taxes with that supports efficient processes for economic growth objectives. This is especially important during periods of economic uncertainty, when businesses need clear and efficient procedures to manage trade policy changes amid the fluctuating market.

Our team at TaxPrime brings extensive experience from the Directorate General of Taxes, providing us with valuable insight into tax authority perspectives and audit procedures. This understanding of both taxpayer and examiner viewpoints enables us to assist companies effectively throughout the tax audit process, from preparation and documentation strategies to representation during examinations and dispute resolution when necessary.